I stopped scrolling on my commute home. The headline said "AI Is Accelerating the Climate Crisis" — right below it was another story: "AI Is the Key to Solving the Climate Crisis." Same day. Same section.

Which one is right? Or are both?

I dug through the data. IEA reports, Goldman Sachs research, MIT papers, Waterloo/Georgia Tech studies, Nature journal articles, and Big Tech sustainability disclosures — and what became clear is that both claims are simultaneously true. They just operate on different timelines. Right now AI is adding carbon. After 2030, the weight shifts toward AI reducing it. The key question is when the crossover happens. And that timing matters quite a bit for investors.

Why Google Abandoned Its Carbon-Neutral Target

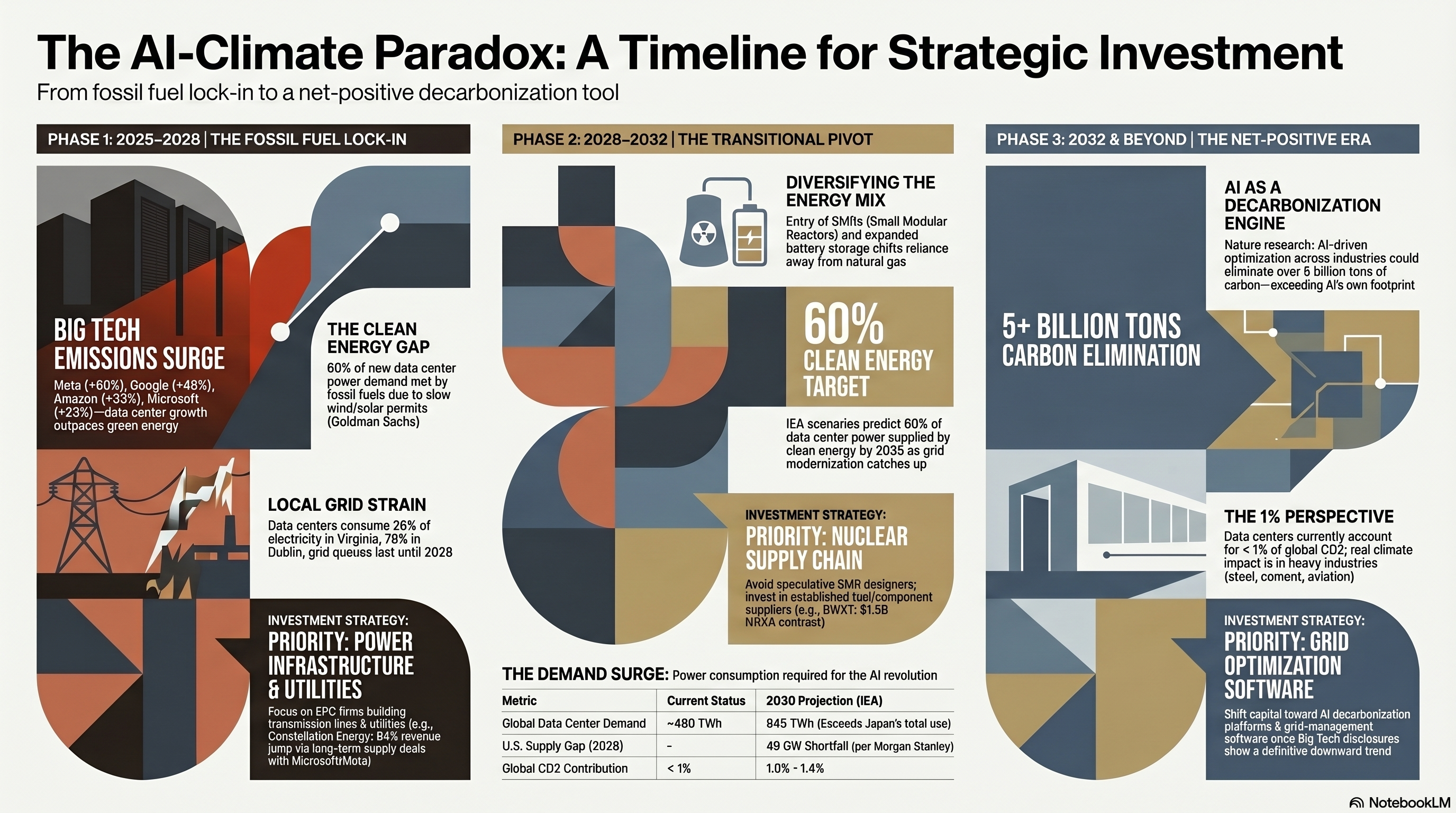

Start with the numbers. Google +48%, Amazon +33%, Microsoft +23%, Meta +60%. These are the actual disclosed emissions figures from companies that pledged carbon neutrality by 2030.

The reason: data center construction is outpacing clean energy deployment. Data centers need power now. Wind and solar permits take years. The only thing that can fill the gap is natural gas. Goldman Sachs estimates that 60% of incremental data center power demand is met by fossil fuels.

The IEA projects global data center power demand will reach 945 TWh by 2030 — more than double today's level, roughly Japan's entire electricity consumption. MIT put it bluntly: "Clean energy cannot keep up with the pace of data center construction." Virginia's data centers consume 26% of the state's electricity. Dublin, Ireland: 79%. Grid interconnection queues are reportedly full through 2028.

But the Claim That AI Reduces Carbon Isn't Wrong Either

A Waterloo/Georgia Tech research team came to the opposite conclusion: AI's energy consumption has minimal impact at national or global scale, and AI could actually accelerate green technology development. IEA data echoes this — data center CO₂ currently accounts for less than 1% of global emissions.

Research published in Nature went further: AI's contribution to decarbonization could exceed the emissions increase from data centers. Grid optimization, methane leak detection, manufacturing process efficiency, improved renewable energy forecasting. Some studies find AI could eliminate over 5 billion tons of carbon across just three key sectors.

The WEF defined this as a "paradox": technology designed to solve global problems simultaneously consumes enormous energy. The resolution, they argue, lies in AI development and energy transition happening in parallel.

Why Both Arguments Are Simultaneously True

The confusion is understandable — news articles pick one side. But the two claims aren't contradictions. They're stories on different timelines.

Now (2025–2028): The Fossil Fuel Lock-in. Data center construction is happening right now, and clean energy can't keep up. Big Tech emissions disclosures already show this.

Medium term (2028–2032): The Pivot. IEA scenarios show a turning point as renewables and SMRs scale up and the data center energy mix shifts. IEA's base scenario has 60% of data center power coming from clean energy by 2035.

Long term (2032+): The Net-Positive Era. AI decarbonization applications go mainstream. The amount AI contributes to carbon reduction exceeds data center emissions. Conditional, but plausible.

This structure matters because it reveals that "Is AI bad right now?" is the wrong question. The right question is "How long does the bad phase last, and what conditions trigger the transition?"

Where Investors Should Look

Right now, in the 2025–2028 window, the beneficiary is power infrastructure. Constellation Energy closed its Calpine acquisition in January 2026, becoming the largest US power generator, with Q1 revenue up 64% year-over-year. Morgan Stanley projects a 49 GW shortfall in US data center power by 2028. "There's no way to print electrons fast enough" is a phrase making the rounds on Wall Street.

The medium-term bet is nuclear — specifically SMR component and fuel supply chains, not pure-play SMR developers. NuScale has no customers and losses up 160% year-over-year. BWXT, by contrast, signed $1.5B in contracts in mid-2025. Whoever wins the SMR design race, BWXT wins too.

The long-term play is AI decarbonization software and grid optimization platforms. Keep the position small now and scale up when Big Tech emissions disclosures actually show a downward turn — that's the signal, not the narrative.

What to Actually Worry About vs. What You Can Ignore

The narrative that "AI alone will destroy the climate" is overblown. Data centers account for less than 1% of global CO₂.

The real risk is different: the fossil fuel lock-in period lasting longer than expected. If grid interconnection queues stretch further and US renewable energy policy weakens, the 2028 turning point could slip to the early 2030s. That feeds into rising AI operating costs, which connects to Big Tech margin compression.

Buying AI decarbonization companies at inflated future premiums right now is also risky. You'd be purchasing the narrative before the results exist.

The AI-climate story is ultimately a question of timing. It's true that more fossil fuels are being burned today. It's also true that long-term decarbonization contributions could exceed emissions. These claims aren't contradictions — they're on different timetables.

The investor's job isn't to pick the winning narrative. It's to watch for when the transition arrives. The quarter when Big Tech carbon disclosures actually start bending downward. That's the real signal.

If it's still not settled whether AI will save or harm the climate — watching how that race unfolds might be the most honest thing you can do right now.

Analysis date: May 31, 2026 | Sources: IEA, Goldman Sachs, MIT, Waterloo/Georgia Tech, Nature, WEF, company sustainability disclosures